We are happy to welcome three new clients to the Elevation Wealth Partners family this quarter. It’s an honor to serve you and we look forward to many years of working together. Thank you to everyone who continues to recommend our services to friends and family.

In the twelve months since the devastating North Bay fires, Elevation Wealth Partners has donated thousands of dollars to those in need, volunteered at pro-bono financial planning events, and counseled clients faced with difficult financial and life decisions. We are committed to helping Sonoma, Napa, and other Northern California communities rebuild . . . and are never too busy to be a sounding board and voice of reason during these often challenging times.

Our Take on the 3rd Quarter and the Markets So Far this Year

Ten years ago, the global financial crisis was in full swing. Merrill Lynch, Bank of American, Bear Stearns, and a slew of other companies had to be bailed-out (and Lehman Brothers went belly up). Congratulations . . . you survived! In fact, being a client of Elevation Wealth Partners during this time means you’ve probably done pretty darn well. That’s not to say it hasn’t been a rough ride at times (pass the Dramamine!).

Market Summary

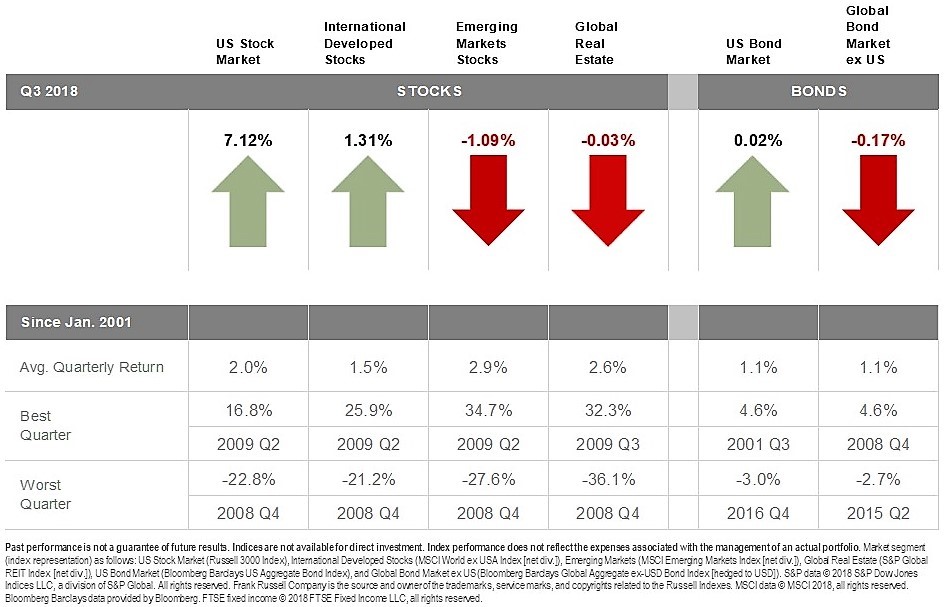

The 3rd quarter was another good quarter for stock investors. The S&P 500 Index closed at an all time high, posting a solid 7.7% total return. Year-to-date, the index is up 10.6%. Small company U.S. stocks (as represented by the Russell 2000 Index) returned 3.6% for the quarter and are up 11.5% for the year thus far.

International stocks continue to largely struggle this year due to tariff re-negotiations, currency moves, and political and economic disruptions. Despite a positive quarter, International Developed Stocks are still down 1.4% on the year and Emerging Markets Stocks are down 7.7%. To emphasize the effect a strengthening U.S. dollar has had on the recent performance of foreign stocks, the same International Developed Stocks Index hedged to the U.S. dollar (that is, without exposure to the ups and downs of foreign currencies) is up 3.2% on the year (a difference of 4.6%) and the Emerging Markets Stocks Index is down just 3.0% on the year (a difference of 4.7%).

Every Elevation Wealth Partners managed account experienced positive returns this past quarter. Furthermore, as we’ve shared in recent client meetings, the majority of the funds and ETFs we invest in have outperformed their stated benchmark and/or category peer year-to-date and over the last year.

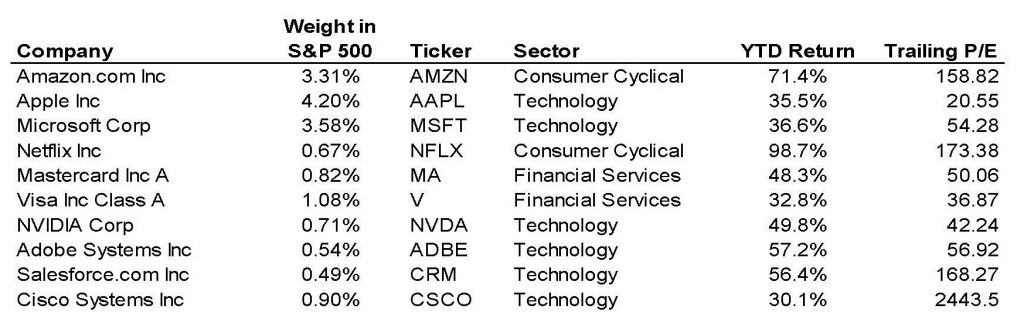

During the quarter, investors drove Apple and Amazon to $1 trillion valuations. Though the results of the general market look promising, looking a little deeper we see that just ten stocks account for half the S&P 500’s gain.

Six of the ten stocks are in the technology sector. Furthermore, the average trailing Price / Earnings Ratio (excluding Cisco) is a lofty 84.6. By comparison, the Dow Jones Industrial Average comprised of 30 blue-chip stocks trails the S&P 500 by more than 2%. Such concentration gives us pause and further reason to eschew cap weighted index funds for value-oriented funds such as those managed by Dimensional Fund Advisors.

Foreign Stocks

Despite a U.S. economy that continues to improve, we believe it is still critical for investors to have a significant allocation towards international equities. In the long run, slowing growth in the U.S. and a rising trade deficit could cause the dollar to fall, amplifying the return on international equities. We believe, despite some hiccups, economic growth continues to improve in both developed and emerging economies and will eventually boost corporate earnings.

We call the chart below the “Dragon” chart because it reminds us of a dragon you would see in a Chinese New Year parade, with the right side of the chart (where the two lines diverge) representing its open mouth. Broad valuation measures suggest that international stocks are simply cheaper, both relative to U.S. stocks and relative to their own long‐term history. Additionally, in the past when the performance of U.S. stocks (as represented by the grey line) and foreign stocks (as represented by the purple line) have diverged with one significantly outperforming the other (such as U.S. stocks from 1997 – 2003), the trend eventually reverses itself and the other outperforms (as Foreign stocks did from 2003 – late 2007). Given the current return spread with U.S. stocks having outperformed foreign stocks by more than 200% since 2011, we are very bullish about foreign stocks over the next decade. For these reasons, we have a full allocation to foreign stock in client portfolios (30% – 40% of a client’s equity allocation).

The Fed and Inflation

The Federal Reserve hiked interest rates another quarter point in September, the third time this year and the eighth rate hike since December 2015. The current pace of rate hikes is the most gradual in the Fed’s history. This coupled with low inflation is the main reason we have no concern about the performance of our chosen bond fund investments even though several are slightly down this year.

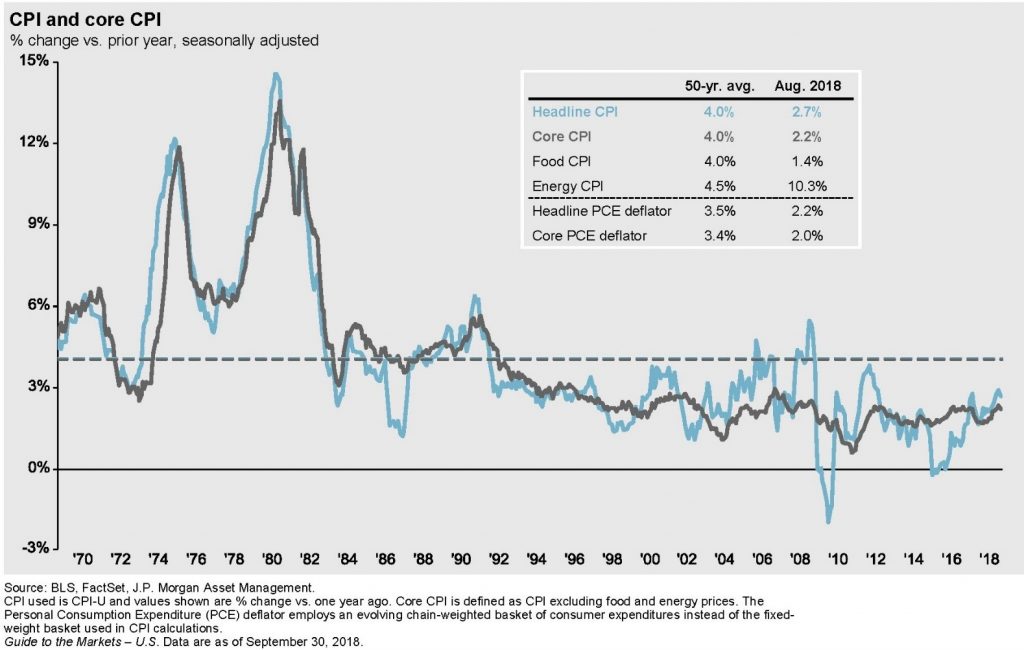

Almost 10 years of monetary stimulus, economic growth and falling unemployment have succeeded in boosting home prices, bond prices and stock prices. However, looking at the chart below, they have not had a meaningful impact on consumer prices. In August, the overall consumer price index was up 2.7% year‐over‐year. While the core index, which excludes food and energy, was up 2.2%. The main difference between the two measures comes from the behavior of energy prices which rose by more than 10% in the year ended in August.

Given record low unemployment, wage growth, and heightened consumer spending, Core CPI is very close to the Federal Reserve’s 2% target. We cannot overstate enough how low inflation is a boon for investors. Depending on the time period, inflation has averaged 3% – 4% a year. Over the last 20 years it has averaged just 2.1% a year. Go back 30 years and all the way back to 1926, inflation has averaged 3% a year. Go back 50 years (and include the hyperinflationary 1970’s), inflation has averaged 4% a year. One of the keys to successful long-term investing is generating returns above and beyond inflation (what is referred to as “real returns”). Generating real returns is one of the most important goals of investing. Should your investments fail to keep up with inflation, not only do you lose purchasing power, you also increase the likelihood you will run out of money over time.

Most financial planners (ourselves included) use 3% inflation in the financial plans and projections we do for clients. However, if you were to experience just 2% inflation instead, it would have the same effect on your financial well-being as earning an extra 1% on your investments. For example, if investment returns are low over the next decade (which they very well could be given the heightened level at which U.S. stocks currently trade), that might not be problematic if inflation is low as well. There are a lot of reasons to believe the Fed will actually be successful at keeping core inflation around 2.0%. However, assuming 2.5% – 3.0% inflation in your financial projections is still the most prudent approach at this time.

Looking Forward

Using the CAPE Shiller P/E Ratio as a guide, we have some concern about the current elevated level of stock prices. A correction does not seem imminent. However, we may very well experience lower than average U.S. stock returns over the next decade.

We resist the notion that “this time is different” with regards to the aforementioned, high-priced growth stocks and continue to favor value stocks.

Expect stock volatility to pick up. . . which is a good thing for investors that can remain disciplined.

Construct global diversified portfolios with a healthy allocation to foreign stocks and bonds.

John Davis retiring at the end of the year.

It is with mixed emotions we announce that our dear colleague John Davis will be retiring at the end of the year. For the last 12 years, John has been an invaluable asset to our clients and a true joy to work with. His professionalism, sincerity, sense of humor, and love of music will be missed.

Sincerely,

Sources: Morningstar, Inc., Dimensional Fund Advisors, J.P. Morgan, Inc. and Dr. David Kelly, Blackrock, Inc.

All investing is subject to risk, including the possible loss of the money you invest. Past performance is no guarantee of future returns. Diversification does not ensure a profit or protect against a loss in a declining market. There is no guarantee that any particular asset allocation or mix of funds will meet your investment objectives or provide you with a given level of income. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index.

3rd Quarter 2018 Market & Investment Commentary

We are happy to welcome three new clients to the Elevation Wealth Partners family this quarter. It’s an honor to serve you and we look forward to many years of working together. Thank you to everyone who continues to recommend our services to friends and family.

In the twelve months since the devastating North Bay fires, Elevation Wealth Partners has donated thousands of dollars to those in need, volunteered at pro-bono financial planning events, and counseled clients faced with difficult financial and life decisions. We are committed to helping Sonoma, Napa, and other Northern California communities rebuild . . . and are never too busy to be a sounding board and voice of reason during these often challenging times.

Our Take on the 3rd Quarter and the Markets So Far this Year

Ten years ago, the global financial crisis was in full swing. Merrill Lynch, Bank of American, Bear Stearns, and a slew of other companies had to be bailed-out (and Lehman Brothers went belly up). Congratulations . . . you survived! In fact, being a client of Elevation Wealth Partners during this time means you’ve probably done pretty darn well. That’s not to say it hasn’t been a rough ride at times (pass the Dramamine!).

Market Summary

The 3rd quarter was another good quarter for stock investors. The S&P 500 Index closed at an all time high, posting a solid 7.7% total return. Year-to-date, the index is up 10.6%. Small company U.S. stocks (as represented by the Russell 2000 Index) returned 3.6% for the quarter and are up 11.5% for the year thus far.

International stocks continue to largely struggle this year due to tariff re-negotiations, currency moves, and political and economic disruptions. Despite a positive quarter, International Developed Stocks are still down 1.4% on the year and Emerging Markets Stocks are down 7.7%. To emphasize the effect a strengthening U.S. dollar has had on the recent performance of foreign stocks, the same International Developed Stocks Index hedged to the U.S. dollar (that is, without exposure to the ups and downs of foreign currencies) is up 3.2% on the year (a difference of 4.6%) and the Emerging Markets Stocks Index is down just 3.0% on the year (a difference of 4.7%).

Every Elevation Wealth Partners managed account experienced positive returns this past quarter. Furthermore, as we’ve shared in recent client meetings, the majority of the funds and ETFs we invest in have outperformed their stated benchmark and/or category peer year-to-date and over the last year.

During the quarter, investors drove Apple and Amazon to $1 trillion valuations. Though the results of the general market look promising, looking a little deeper we see that just ten stocks account for half the S&P 500’s gain.

Six of the ten stocks are in the technology sector. Furthermore, the average trailing Price / Earnings Ratio (excluding Cisco) is a lofty 84.6. By comparison, the Dow Jones Industrial Average comprised of 30 blue-chip stocks trails the S&P 500 by more than 2%. Such concentration gives us pause and further reason to eschew cap weighted index funds for value-oriented funds such as those managed by Dimensional Fund Advisors.

Foreign Stocks

Despite a U.S. economy that continues to improve, we believe it is still critical for investors to have a significant allocation towards international equities. In the long run, slowing growth in the U.S. and a rising trade deficit could cause the dollar to fall, amplifying the return on international equities. We believe, despite some hiccups, economic growth continues to improve in both developed and emerging economies and will eventually boost corporate earnings.

We call the chart below the “Dragon” chart because it reminds us of a dragon you would see in a Chinese New Year parade, with the right side of the chart (where the two lines diverge) representing its open mouth. Broad valuation measures suggest that international stocks are simply cheaper, both relative to U.S. stocks and relative to their own long‐term history. Additionally, in the past when the performance of U.S. stocks (as represented by the grey line) and foreign stocks (as represented by the purple line) have diverged with one significantly outperforming the other (such as U.S. stocks from 1997 – 2003), the trend eventually reverses itself and the other outperforms (as Foreign stocks did from 2003 – late 2007). Given the current return spread with U.S. stocks having outperformed foreign stocks by more than 200% since 2011, we are very bullish about foreign stocks over the next decade. For these reasons, we have a full allocation to foreign stock in client portfolios (30% – 40% of a client’s equity allocation).

The Fed and Inflation

The Federal Reserve hiked interest rates another quarter point in September, the third time this year and the eighth rate hike since December 2015. The current pace of rate hikes is the most gradual in the Fed’s history. This coupled with low inflation is the main reason we have no concern about the performance of our chosen bond fund investments even though several are slightly down this year.

Almost 10 years of monetary stimulus, economic growth and falling unemployment have succeeded in boosting home prices, bond prices and stock prices. However, looking at the chart below, they have not had a meaningful impact on consumer prices. In August, the overall consumer price index was up 2.7% year‐over‐year. While the core index, which excludes food and energy, was up 2.2%. The main difference between the two measures comes from the behavior of energy prices which rose by more than 10% in the year ended in August.

Given record low unemployment, wage growth, and heightened consumer spending, Core CPI is very close to the Federal Reserve’s 2% target. We cannot overstate enough how low inflation is a boon for investors. Depending on the time period, inflation has averaged 3% – 4% a year. Over the last 20 years it has averaged just 2.1% a year. Go back 30 years and all the way back to 1926, inflation has averaged 3% a year. Go back 50 years (and include the hyperinflationary 1970’s), inflation has averaged 4% a year. One of the keys to successful long-term investing is generating returns above and beyond inflation (what is referred to as “real returns”). Generating real returns is one of the most important goals of investing. Should your investments fail to keep up with inflation, not only do you lose purchasing power, you also increase the likelihood you will run out of money over time.

Most financial planners (ourselves included) use 3% inflation in the financial plans and projections we do for clients. However, if you were to experience just 2% inflation instead, it would have the same effect on your financial well-being as earning an extra 1% on your investments. For example, if investment returns are low over the next decade (which they very well could be given the heightened level at which U.S. stocks currently trade), that might not be problematic if inflation is low as well. There are a lot of reasons to believe the Fed will actually be successful at keeping core inflation around 2.0%. However, assuming 2.5% – 3.0% inflation in your financial projections is still the most prudent approach at this time.

Looking Forward

Using the CAPE Shiller P/E Ratio as a guide, we have some concern about the current elevated level of stock prices. A correction does not seem imminent. However, we may very well experience lower than average U.S. stock returns over the next decade.

We resist the notion that “this time is different” with regards to the aforementioned, high-priced growth stocks and continue to favor value stocks.

Expect stock volatility to pick up. . . which is a good thing for investors that can remain disciplined.

Construct global diversified portfolios with a healthy allocation to foreign stocks and bonds.

John Davis retiring at the end of the year.

It is with mixed emotions we announce that our dear colleague John Davis will be retiring at the end of the year. For the last 12 years, John has been an invaluable asset to our clients and a true joy to work with. His professionalism, sincerity, sense of humor, and love of music will be missed.

Sincerely,

Sources: Morningstar, Inc., Dimensional Fund Advisors, J.P. Morgan, Inc. and Dr. David Kelly, Blackrock, Inc.

All investing is subject to risk, including the possible loss of the money you invest. Past performance is no guarantee of future returns. Diversification does not ensure a profit or protect against a loss in a declining market. There is no guarantee that any particular asset allocation or mix of funds will meet your investment objectives or provide you with a given level of income. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index.