We are happy to welcome three new clients this quarter. It’s an honor to serve you and we look forward to many years of working together. Thank you to everyone who continues to recommend our services to friends and family. We are also pleased to announce the addition of Kelly Gillette to Elevation Wealth Partners. Kelly will be working closely with John Davis in the Santa Rosa office as a Client Service Advisor. Prior to joining ZRC, worked Kelly worked for a number of North Bay companies in client facing roles including REACH Air Medical Services and Charles Schwab & Co.

4th Quarter Commentary

Stocks continued their climb higher in the fourth quarter as the tax bill became reality and as generally upbeat economic data gave the green light to the Fed to raise rates again. The S&P 500 Index rose over 6% during the quarter and gained over 21% for the year. In fact, all broad equity asset classes returned double digits for the year with Emerging Markets stocks leading the way and gaining more than 37%. Even the most conservative Elevation Wealth Partners managed accounts posted low double-digit gains in 2017 and the most aggressive managed accounts (with 100% stocks) returning upwards of 20%.

Investment Implications of the Tax Cut and Jobs Act and 2018 Economic & Market Outlook

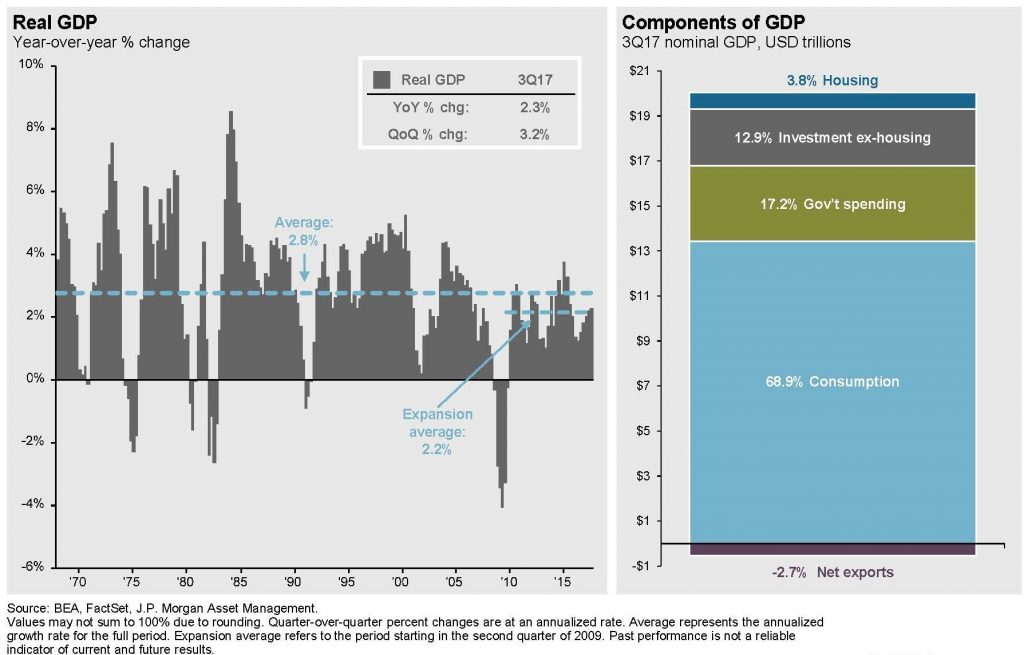

The economic expansion continues at a slow but steady pace. The U.S. enters 2018 with solid growth, having logged real GDP gains of better than 3% in the middle two quarters of 2017 (see chart on next page). In its ninth year, the expansion is the third longest since 1900. This momentum should continue into 2018 with real GDP gains in excess of 3% in the first half of the year, fueled in part by a boost to consumer spending from tax cuts and a strong global economy.

In broad terms, before accounting for either the interest costs on increased debt incurred or the dynamic effects on revenues and spending caused by the impact of the act on the economy, the total cost of the act over 10 years is estimated to be $1.456 trillion. The tax cuts are heavily front loaded, with 62% of the benefits occurring in the first four years. This is partly because of the expiration of the individual tax cuts in December of 2025. Given this, it seems reasonable to assume that 60% of the tax cut flows through directly to higher consumer spending in 2018 and 50% in 2019. In an economy of $20 trillion, these gains could add 0.6% to GDP growth in 2018, and a further 0.3% in 2019.

Unemployment continues to fall, which should drive up wages. While the economy maintains a slow-but-steady pace of growth, the labor market has continued to tighten. This reflects two key trends: Low productivity growth, which implies most GDP growth has to come from employing more workers, and low labor force growth, which means that much of the job growth has come from re-employing the unemployed rather than new workers entering the labor market.

Solid GDP growth in 2017 and 2018 should cut the unemployment rate further, perhaps to 3.5% by the end of 2018, having already fallen close to 4% by the end of 2017. While wages have been slow to react to a tight labor market so far, extra pressure to find workers spurred by tax cuts could finally boost wage growth in 2018.

International stocks may offer better opportunities. Earnings prospects look more promising overseas. The Eurozone is growing particularly fast, thanks to a still undervalued currency, rising confidence and considerable pent-up demand, while other developed markets like Japan, Canada and the U.S. continue to accelerate. The UK appears to be weathering the impact of the Brexit vote better than many had feared, thanks to more competitive exports on a weaker currency. Meanwhile, a rebound in demand for commodities continues to be a positive for Latin America, Canada and Australia. U.S. earnings in the next 12 months are expected to be at a record high. However, earnings in Europe remain far below their pre-financial crisis peaks, while Emerging Markets earnings are below peaks achieved in 2011. A long cyclical recovery in Europe and an improving banking system should lift European earnings while EM profits should rebound on firmer commodity prices. Both European and EM earnings appear to have more room to grow than in the U.S.

While U.S. P/E ratios are above their 25-year average, Europe and EM look more attractive from a valuation perspective: European P/Es are somewhat lower. Meanwhile, EM Price-to-Book ratios remain at just average levels. If, in the long run, the U.S. dollar falls to more reasonable levels, this could add to the returns on (unhedged) international equities.

Looking forward, higher valuations and uncertainty underscore the need for broad diversification and careful portfolio management. We still see plenty of risks (from geopolitical to cryptocurrencies). Cutting the corporate tax rate from 35% to 21% will take the U.S. from having the highest corporate tax rates in the OECD to something close to the global average. A lower corporate tax rate should boost investment spending by improving the internal rate of return on investments made today, compounded by the new ability to completely expense capital spending. But spending may not be boosted by as much as some expect: the U.S. economic expansion is old and long-term growth prospects are subdued. The net benefit to corporations of corporate tax cuts should be roughly $80 billion per year over the next few calendar years. One simple assumption might be that companies spend roughly $40 billion of this on capital spending and their workforce and return the other $40 billion to shareholders who, in turn spend half of their windfall, providing, between investment and consumption.

The Fed will keep raising interest rates. The global economy is generating fewer worries than in recent years and the U.S. is approaching or at many long-term targets, like unemployment and inflation, making it clear that interest rates are still too low. The decision to increase rates in December reflected this conclusion, and barring any significant negative shocks or fiscal stimulus, we anticipate the Fed to further raise rates by 0.25% at least three times in 2018, with upside risk to four, despite recent personnel turnover. In addition, the FOMC’s plan to reverse quantitative easing, the start of which was announced at the Fed’s September meeting and commenced shortly after, demonstrates that the central bank is committed to raising interest rates across the yield curve.

From a big picture perspective, stronger growth should favor stocks over bonds. 529 plans could also look more attractive given a new provision for their use in K-12 private education. The building industry may be negatively impacted by reductions to deductions for state and local taxes and mortgage interest. The health care sector could be a very mixed bag, with highly taxed pharmaceutical companies benefiting but hospitals and insurance companies being negatively impacted by the end of the individual Affordable Care Act mandate.

If it has been some time since we reviewed your financial goals or something has changed in your financial life (you have been granted stock in your company, changed jobs, lost a loved one, or are nearing retirement) – please contact us to schedule a meeting. As always, we are here to be a resource to you and those important to you.

Sincerely,

Barry N. Mendelson, CFP John L. Davis, CFP Richard P. Clarke, CPA, PFS

Ryan K. Kosakura, CFA Kelly Gillette

Sources: J.P. Morgan Asset Management and Morningstar, Inc.

All investing is subject to risk, including the possible loss of the money you invest. Past performance is no guarantee of future returns. Diversification does not ensure a profit or protect against a loss in a declining market. There is no guarantee that any particular asset allocation or mix of funds will meet your investment objectives or provide you with a given level of income. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index.