With summer and camping trips in full swing and U.S. stocks hovering around bear market territory (i.e., down more than 20%) we thought it was timely to share some tips on how to plan for and survive an encounter with a bear (whether it be the furry or financial kind).

Plan for your adventure

Seasoned campers know that a successful trip starts with the preparation long before loading up the car. You’ll need to consider how long you’ll be camping, where you’re going, and what weather you might encounter. Of course, if you’re heading into unfamiliar territory, it’s good to check with a local guide to make sure you prepare appropriately. The goal is to make sure you are well-equipped for the planned … and unplanned.

Similarly, at Elevation Wealth Partners, we help you plan for your next financial adventure by taking inventory of what you have, assessing the financial terrain, and creating your personal financial plan to chart a path toward achieving your goals … just like taking a good map and compass along on your camping trip.

Your Investment Policy Statement explains what you can expect given your asset allocation (i.e., what proportion of your investments are in stocks and bonds). And, as with camping, it’s a good idea to have access to extra financial resources should you need additional provisions. We recommend maintaining an emergency supply of cash to carry you through three to six months of living expenses.

Know how to read your surroundings

Just like an outdoor adventure, it’s good to understand the conditions you might encounter along your financial journey.

During the first quarter, Gross Domestic Product contracted by an annualized rate of -1.6%, recording the first negative reading since the first half of 2020. The unemployment rate continues to hold steady with a reading of 3.6% in May 2022 . . . which is very low by historical standards. This coincides with a tight labor market that saw approximately 11.4 million job openings for 6 million unemployed workers at the end of April. The Fed’s preferred gauge of overall inflation, the core Personal Consumption Expenditures (PCE), reported 4.7% inflation in May 2022, well above the Fed’s long-term target average of 2.0%. Headline inflation, as measured by the Consumer Price Index (CPI), closed out May with a reading of 8.6%. These readings tend to differ primarily because CPI includes volatile categories like food and energy in its methodology while core PCE does not.

U.S. interest rates increased during the quarter as the Federal Reserve raised the target range of the Fed Funds rate twice from 0.25%-0.50% to 0.75%-1.00% in May and then again to 1.50%-1.75% in June. The second rate hike of 0.75% was the single largest rate hike approved by the Fed since 1994. However, markets have currently priced in the expectation of seven additional rate hikes during the remainder of 2022, with an implied target range of 3.25%-3.50% by year’s end.

The U.S. Dollar Index, a measure of the value of the United States dollar relative to a basket of foreign currencies, increased 6.5% in the second quarter. Over the past 12 months, the U.S. dollar increased by 13.3%. The increase in the dollar is a headwind to non-U.S. investments held by U.S. investors for the last 12 months.

After the strong global rebound that followed the market downturn associated with the onset of the COVID-19 pandemic, both stock and bond markets have been more volatile than usual in 2022. The first quarter ended with U.S. stocks trending downward and interest rates trending upward. And, generally speaking, the trends accelerated in the second quarter.

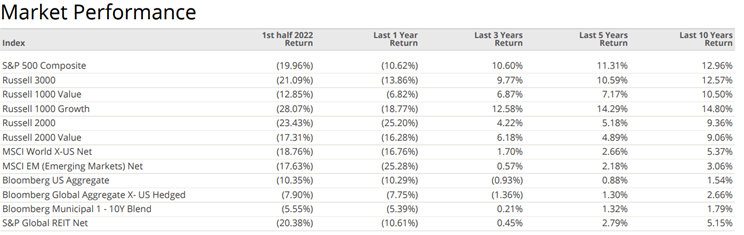

The S&P 500 index, a popular headline stock market index in the U.S., suffered its worst first-half calendar year performance in decades while bond markets continued their descent fueled by the expectation of continued rate hikes. Elevated inflation readings and the looming specter of recession along with other market influences resulted in negative performance for the quarter across all major asset classes.

For the quarter, U.S. stocks (as measured by the Russell 3000 Index) lost 16.7%, and non-U.S. developed market stocks (as measured by the MSCI World Ex U.S. Index) lost 15.2%. Emerging market stocks (as measured by the MSCI Emerging Markets Index) lost 12.1%. Compounded by the first quarters woes, the Russell 3000 Index returned -21.09% and the S&P 500 Composite returned -19.96% in the first half of 2021. Even with those big drops, the Russell 3000 still reported a respectable 9.77% 3-year annual average increase, and the S&P 500 Composite reported a 10.60% 3-year average annual increase.

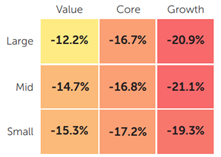

U.S. Stocks – Q2 2022

In the United States value stocks declined less than growth stocks in all size categories. In addition, large-cap stocks declined less than small cap stocks in all style categories with the exception of growth stocks.

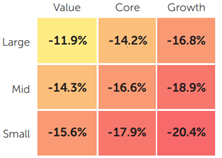

International Stocks – Q2 2022

In developed international markets, large-cap stocks declined less than small-cap stocks in all style categories for the quarter. And like in the U.S., value stocks declined less than growth stocks in all size categories.

Bonds

Bonds serve as the foundational bedrock upon which your portfolio is built. They’re meant to provide a cushion of modestly positive returns to your portfolio when stock markets are down. But, due to significant interest rate increases this year, bond prices have fallen, giving investors a double whammy, with negative returns in both stock and bond markets. So far this year, bonds haven’t provided the safety net we had hoped for, and their performance has varied across different areas of bond markets.

What to do in a close encounter with a bear

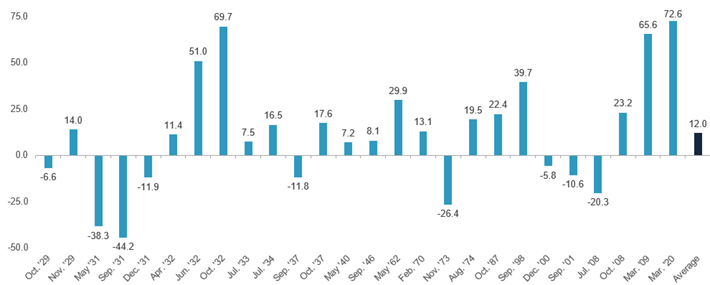

Should you find yourself encountering a real-life bear in the wilderness, your best course of action is to stay calm and stand your ground. Experts advise to not make any sudden movements that the bear might find threatening. While it could be unnerving for you personally, statistics prove that most bear encounters end without injury. The same holds true for your investments. Selling during a down-market could be very difficult to recover from. Bear markets are normal. There have been 26 bear markets in the S&P 500 since 1928. However, there have also been 27 bull markets. And stocks have risen significantly over the long term.

U.S. Stock Market – 1 Year Total Returns Following 20% Drop

The Silver Lining

With stocks and bonds trading at much lower prices, one could argue they are “on sale.” The price-to-earnings ratio for U.S. stocks, a measure of how much a dollar of earnings costs on average, has gone from 23.9 at the beginning of the year to 19.1 at the end of May. Bond yields are also higher than they have been for a few years, with the five-year Treasury bond yield near 2.9% compared to less than 1.4% at the start of the year. That means stocks and bonds are now a better value—and we expect greater potential for future returns.

For many of our clients, we have already taken advantage of the price changes by:

- Rebalancing accounts to “buy low and sell high,” allowing us to move more money into the asset classes that are relatively cheaper now.

- Tax-loss harvesting by selling investments for a loss while moving into a different fund that has a similar strategy. This may reduce your tax bill.

Here’s some other ideas that can help you take advantage of the down market.

- Increase your contributions – If you’re already contributing to your company retirement plan, IRA, or trust account consider increasing the amount. Adding more money now means you can benefit from the recovery when it occurs.

- Convert an IRA to a Roth – With prices down, this may be a good time to convert a traditional IRA to a tax-free Roth IRA. This could allow the market recovery to be captured in a tax-free account.

- Set up a 529 Plan – If you plan to help your children or grandchildren with future education expenses, consider establishing a 529 plan for them — or adding to it if you already have one. Your contributions can take advantage of lower prices.

Looking Forward

During periods like the first half of this year, it’s natural to be nervous about markets and wonder about your financial plans. Keep these points in mind with a long-term, forward-looking perspective:

- The risk and return experience so far this year for most asset allocations is within the range of potential downside risk that we consider in the financial plans that we create for clients.

- Inflation is expected to moderate to more normal levels.

- Interest rates have increased substantially in 2022, even before the Federal Reserve announced rate increases.

So, enjoy your summer knowing that odds-are, you will not have to worry about bears. And, if you’re still concerned, be sure to reach out to your Elevation Wealth Partners or anyone on the Elevation Wealth Partners

Important deadlines and dates for the upcoming quarter.

September 5 ……… Labor Day – The financial markets are closed and so are Elevation Wealth Partners offices

September 11…….. Grandparents Day

September 15 ……. Estimated Tax Payment for 3rd Quarter of 2022 (Form 1040-ES)

September 15 ……. Final deadline to file partnership and S-corporation tax returns for tax year 2021, if an extension was requested (Forms 1065 and 1120-S)

October 17 ……….. Final extended deadline (if previously requested) to file individual and corporate tax returns for the year 2021 using Form 1040 and Form 1120

October 17 ……….. Contribute to Solo 401(k) Plan or Simplified Employee Pension (SEP) Plan for 2021 by Self-Employed if you filed a Form 1040 extension

As always, we are grateful for the opportunity to serve you and your loved ones. If you know of others who could benefit from a conversation with us, please do not hesitate to make the connection. We would be more than happy to provide a complimentary consultation.

To schedule a 30-minute meeting with Barry Mendelson, CFP® – Wealth Advisor & Financial Planner https://calendly.com/zrc-barry-m/meet-with-barry

To schedule a 30-minute meeting with Kevin Goulding, CFP® – Wealth Advisor & Financial Planner https://calendly.com/kevin-goulding/meet-with-kevin

Sources: Dimensional Fund Advisors, Buckingham Strategic Partners, Blackrock, Inc. All investing is subject to risk, including the possible loss of the money you invest. Past performance is no guarantee of future returns. Diversification does not ensure a profit or protect against a loss in a declining market. There is no guarantee that any particular asset allocation or mix of funds will meet your investment objectives or provide you with a given level of income. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index.