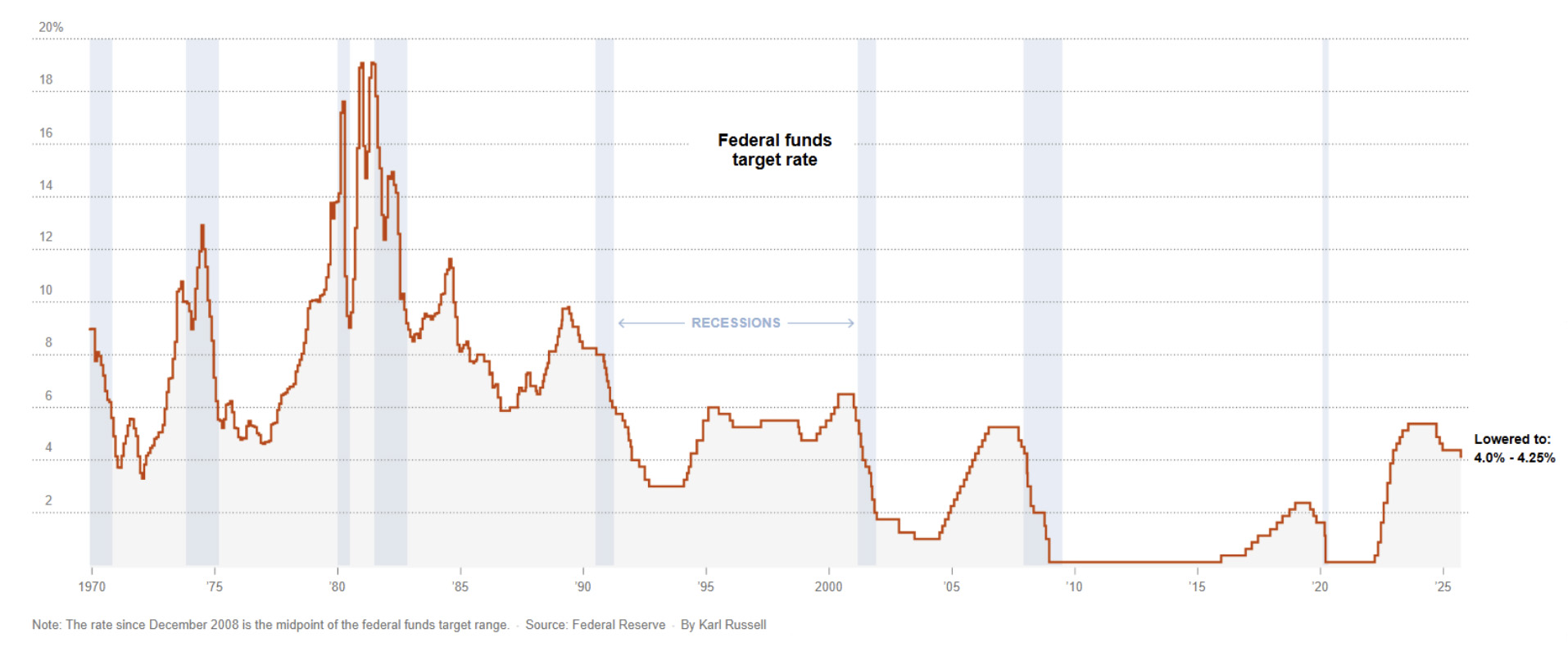

On September 17, the Federal Reserve cut interest rates by 0.25%—its first move in 2025 after a full percentage point of cuts in 2024. Fed Chair Jerome Powell described the situation as “challenging,” with inflation rebounding over the summer due to tariffs, while the labor market remains solid but shows early signs of strain. Two more cuts may follow, with meetings scheduled for October and December.

Soft Landing or Recession Warning?

Investors must ask: Is this a routine adjustment or a sign of trouble? Historically, rate cuts have led to two outcomes:

- Soft landing (44%): The Fed cuts rates from strength, and the economy keeps growing.

- Recession response (56%): Cuts come as a reaction to economic downturns.

This distinction matters. Bonds tend to rally either way, but stocks perform better when cuts are proactive, not reactive.

Current Signals Point to Recalibration

Today’s data suggests the Fed is recalibrating, not panicking:

- GDP growth is slowing but remains positive.

- Inflation has eased, though still above the 2% target.

- Unemployment is low.

- The yield curve has steepened—typical during rate cuts, not a red flag.

This points to a cooling economy finding balance, not one in crisis.

The Fed’s Forecasts

The Fed’s “dot plot” reveals internal disagreement:

- One hawk wants rates to stay at 4.25–4.5%.

- One dove (likely Kevin Miran) sees rates falling to 2.75–3%.

- Most officials expect a middle ground.

Longer-term projections show rates settling around 3% by 2028—the “neutral rate” that supports stable growth.

Why Long-Term Rates Matter More

While the Fed controls short-term rates, long-term rates drive mortgages, corporate bonds, and business loans—and they’re influenced by forces beyond the Fed’s reach:

- AI investment boom: Massive funding needs for infrastructure.

- Government debt: Competes for capital, keeping rates elevated.

- Inflation expectations: Markets remain cautious.

These structural pressures suggest a “higher-for-longer” rate environment compared to the ultra-low rates of the 2010s.

Two Realities for Investors

- Short-term rates: The Fed is cautious, balancing inflation and employment. With inflation above target and immigration slowing, aggressive cuts are unlikely unless the job market worsens.

- Long-term rates: Driven by broader forces—AI, debt, and investor sentiment—these are harder to influence and likely to stay elevated.

What Investors Should Do

- Stock investors: Focus on quality. Companies with strong earnings and balance sheets will fare better. Tech remains attractive if growth is real. Expect volatility.

- Bond investors: Yields are appealing, offering stability and income. Fixed income is more attractive than it’s been in years.

- Everyone: Diversify across asset classes and geographies. This isn’t a crisis—just a shift from restrictive to neutral policy. Stay disciplined and avoid reactive decisions.

Sources: The New York Times, Vanguard, Focus Partners